In anticipation of the upcoming 2024 tax season, it is crucial to proactively prepare for any potential alterations that could affect your tax filing process. Whether you are a seasoned tax filer or venturing into the world of tax filing for the first time, navigating the tax season can be quite daunting.

To ensure a smooth and stress-free experience for the upcoming tax season in 2024, we have curated this indispensable handbook. It will equip you with the necessary information to accurately and efficiently file your tax returns for the year 2023.

2023 Tax Filing Important Dates and Deadlines

Marking the beginning of the 2024 tax cycle, January 23, 2024, signifies the commencement of the official new tax season.

If the tax deadline is approaching and you cannot file your taxes, it is crucial to take the necessary steps to request an extension. One way to do this is by submitting IRS Form 4868, which is known as the Application for Automatic Extension of Time to File U.S. Individual Income Tax Return.

Please be aware that while this affords you extra time for tax filing purposes, it does not grant you an extension for tax payment. Should you be unable to settle your taxes in full by April 15, it is crucial to establish a payment plan with the IRS to prevent any detrimental consequences, including wage garnishment or the imposition of a tax lien.

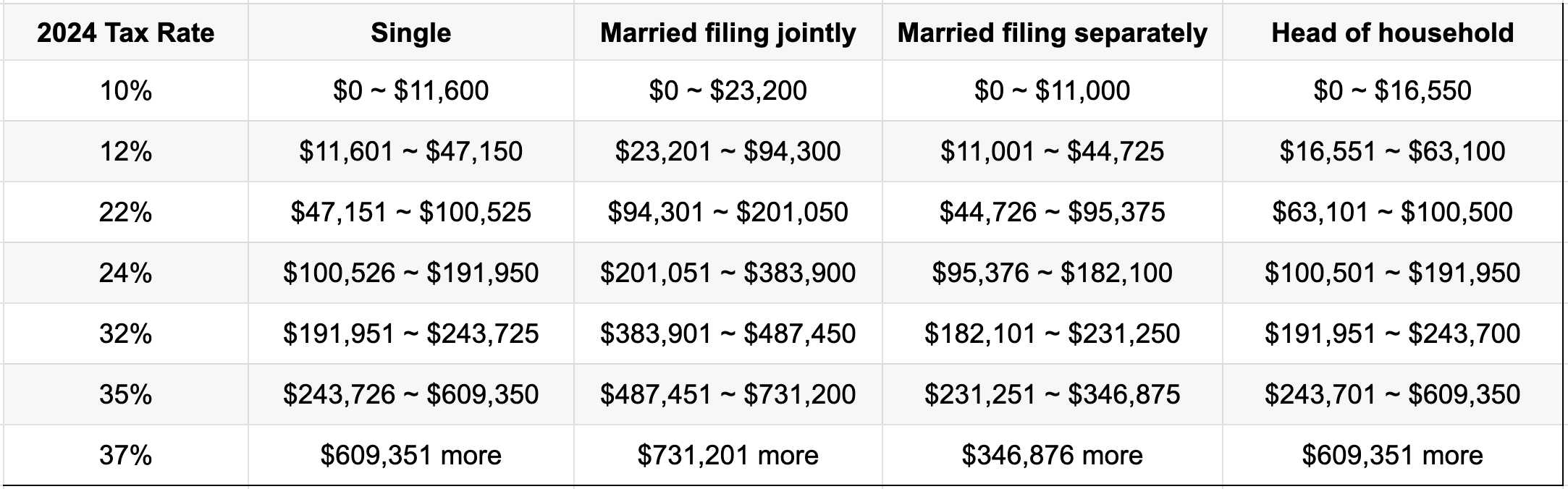

2024 Tax Law Changes and Updates

The upcoming 2023 tax return brings numerous modifications and revisions that might affect your financial situation. Among these alterations, the elevated standard tax deduction is a prominent highlight, as it undergoes regular adjustments to accommodate inflation rates. Individuals filing as single will witness a noteworthy increase of $900, resulting in a new standard deduction of $13,850.

Married individuals filing jointly can take advantage of a higher standard tax deduction for the 2023 tax year. This year, their standard deduction will see a significant increase of $1,800 compared to the previous year, totaling a generous $27,700.

Apart from the rise in the standard deduction, a few other factors could potentially influence your tax situation.

2024 Child Tax Credit

In the upcoming tax year of 2023, the Child Tax Credit will revert to its pre-COVID regulations, just as it did in the previous year of 2022. Consequently, the tax credit will no longer be entirely refundable, only allowing for a refund of up to $1,600.

To be eligible for the full credit, individuals must have a modified adjusted gross income (MAGI) equal to or less than $200,000 ($400,000 or less for those who are married and filing jointly).

2024 Income Tax Credit

In 2024, individuals filing taxes for the 2023 tax year can avail of the Earned Income Tax Credit (EITC), which ranges from $600 to $7,430. The amount eligible for this credit is determined by income level, number of dependents, and tax filing status. If individuals do not have qualifying children, they must be between the ages of 25 and 65 to claim the EITC.

Number of Qualifying Children and Maximum Credit Amount:

- $600 Max Tax Credit with 0 Children

- $3,995 Max Tax Credit with 1 Child

- $6,604 Max Tax Credit with 2 Children

- $7,430 Max Tax Credit with 3+ Children

2024 Annual Gift Tax

In the upcoming year of 2023, individuals can take advantage of the 2024 annual gift tax deduction, allowing them to gift up to $17,000 ($34,000 if married) without incurring any taxes.

Health Savings Account (HSA) in 2024

In the upcoming tax year of 2023, individuals are granted the opportunity to contribute to their Health Savings Account (HAS) up to a maximum of $3,850. This equates to a $200 increase compared to the previous year. For those who have chosen family coverage, the contribution limit is set at $7,750.

The benefits of HSAs are threefold when it comes to taxes:

- Individuals can deduct 100% of their contributions from their tax burden.

- Any interest earned within the HSA remains tax-deferred unless it is used for non-medical expenses.

- When funds are withdrawn for eligible medical expenses, they are entirely tax-free.

2024 IRA & 410(k) Contributions Tax Deduction

In the upcoming year of 2023, individuals who contribute to their 401(k) plans will be thrilled to learn that the annual deferral limits have experienced a significant jump, with up to $2,000 to increase from 2022.

The contribution limits for taxpayers aged 50 or above have been revised, allowing them to increase their investments in traditional and safe harbor 401(k) plans. Specifically, individuals in this age group can now contribute an extra $7,500, a notable increase from the previous year’s limit of $6,500.

In the realm of individual retirement accounts, specifically the traditional and Roth IRA, it is important to note the contribution limit for the year 2023. This limit stands at $6,500, although individuals who have reached the age of 50 or older are allowed to contribute up to $7,500. However, it is crucial to be aware of potential adjustments to your contribution amount in the case of a Roth IRA. These adjustments are dependent on your modified adjusted gross income (MAGI)

2024 Student Loan Interest Tax Deduction

With the resumption of student loan payments and the return of accruing interest, there is a potential opportunity to claim a deduction of up to $2,500 on your 2023 tax return. To be eligible for this deduction, individuals must have a MAGI of less than $90,000 (single, qualifying widow(er), or head of household) or $180,000 if they are married and filing jointly.

Step-by-Step Guide to Filing Taxes in 2024

Once you have assembled the essential paperwork, it is crucial to adhere to the comprehensive tax filing guide provided below. Following these step-by-step instructions will ensure a seamless and accurate procedure.

Opt for a tax preparation approach like utilizing tax preparation software or seeking advice from a tax professional. Should you opt for the traditional paper tax return, it is important to remember that the processing time may extend up to six months. E-filing is strongly recommended whenever feasible.

To ensure the accuracy and completeness of your tax return, it is important to input all relevant information into PriorTax. Remember to sign and date your return and attach any necessary tax documents, forms, and schedules if filing by mail. Remember, the deadline to submit your tax return is April 15.

When managing your taxes, don’t hesitate to contact the experienced Tax Professionals at PriorTax. PriorTax understands the importance of affordable tax preparation for individuals and small business owners, offering services tailored to your specific needs. Additionally, we are dedicated to assisting you in resolving any tax debt issues you may face. Take the first step towards financial peace of mind by connecting with your dedicated Tax Professional, free of charge.