Willem Veldhuyzen

Willem Veldhuyzen  Feb 17, 2026

Feb 17, 2026 What Happens If You File Taxes Late? (and What to Do Right Now)

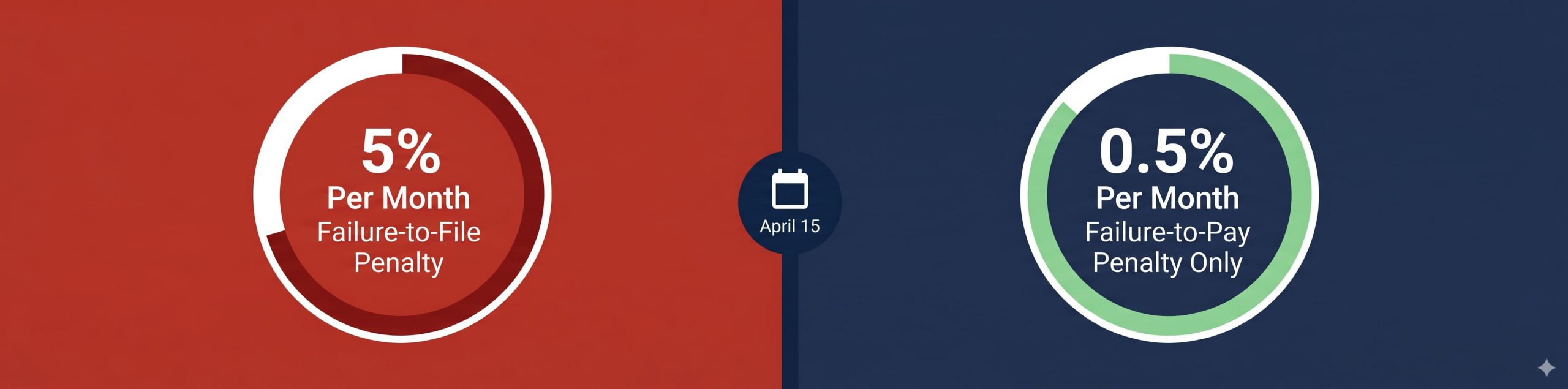

*updated 6-19-2026 Key Takeaways File immediately even without payment to avoid 5% monthly late filing penalty Request extension using Form 4868 if you need six months for paperwork only Set up installment plan via Form 9465 when you cannot pay balance in full Pursue offer in compromise if tax debt exceeds ability to pay without […]

![How to File 2023 Taxes Late [Why Filing Now Beats Waiting Until You Can Pay]](https://blog.priortax.com/wp-content/uploads/2026/06/how-to-file-2023-taxes-late.jpg)

![IRS COVID Penalty Refund [File By July 10 or Lose Your Claim]](https://blog.priortax.com/wp-content/uploads/2026/06/irs-covid-penalty-refund-check.jpg)